INFLATION OUTLOOK –Disinflationary trend to persist in July, 2025

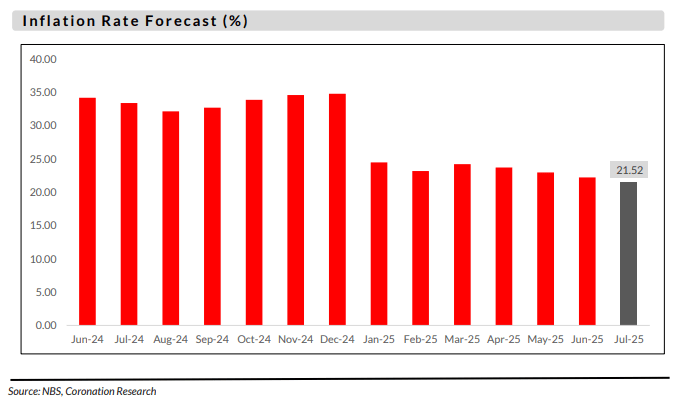

In anticipation of the inflation data release for July on Friday, we foresee the continuation of the disinflationary trend, with the headline inflation rate projected to decrease to 21.52% year-on-year, down from 22.22% year-on-year in June. Concurrently, on a month-on-month basis, we expect a slight increase in headline inflation to 1.80%, as ongoing inflationary pressures in core components such as ICT and transport are likely to surpass the rate of moderation in food inflation.

Forecast

Our inflation forecast for July 2025 is based on four primary factors. First, the passthrough effect of the CBN’s foreign exchange policy reforms continues to bolster Naira stability. Although July experienced a slight depreciation of the Naira against the US Dollar by 0.46%, compared to a 3.02% appreciation in June 2025, it closed at ₦1,534/USD. Second, domestic energy costs have decreased as petrol prices fell below ₦900 per litre; however, rising logistics costs (transport activities) have partially countered this decline. Third, we have noted a minor reduction in prices for certain farm produce due to early harvests in some agricultural regions. Finally, favorable base effects continue to serve as a significant disinflationary catalyst, maintaining the downward trend in headline CPI at least on a year-on-year basis.

The inflation outlook for August points to a potential moderation, supported by continued foreign exchange stability and a

slight easing in food prices from the ongoing early harvest season. If the current FX stability persists and early harvest gains

are sustained, headline inflation could remain broadly in line with July’s level. However, risks to this outlook include a sharp

depreciation of the naira from external shocks, an increase in fuel prices from potential global geo-political risks, and

upward pressure on food prices stemming from recent flooding in Nigeria, which has impacted farmlands and disrupted

transportational nodes needed for logistics. These factors could reverse the current disinflationary trend and move

inflation above 22% y/y or limitthe pace of moderation relative to the previous month. SPOURCE: CORONATION MERCHANT BANK