Nigeria Stock Market Trading Activities on January 3, 2023: Markets starts with N187.90 billion gain

Nigerian stocks began the year on a positive note as the NGX All Share Index (ASI) increased by 1.89% to

Read MoreBusiness news and information and Latest Nigeria News Today

Nigerian stocks began the year on a positive note as the NGX All Share Index (ASI) increased by 1.89% to

Read More

Nigeria is the first nation in Africa to secure partnership for the deployment of Elon Musk’s Starlink. Before the year’s

Read More

On 28 December, 2022, it was reported that the National Assembly had passed the annual Finance Bill 2022 (the Bill),

Read More

The Federation of International Football Associations (FIFA) says it will ask countries to name a stadium in their domain in

Read More

After joining the European Union (EU) about ten years ago, Croatia has reached two significant milestones: the adoption of the

Read More

The Managing Director of the International Monetary Fund (IMF), Kristalina Georgieva, has predicted that a third of the global economy

Read More

On Sunday, Dubai eliminated its 30% tax on alcohol sales in the sheikhdom and made the needed liquor licenses freely

Read More

The 2023 Tony Elumelu Foundation Entrepreneurship Programme application portal is now open and will run till March 31, 2023. Entrepreneurs

Read More

The Tony Elumelu Foundation Entrepreneurship Program has opened its application window for its 8th cycle, the 2023 edition. African businesspeople

Read More

The 2023 round of the Tony Elumelu Foundation Entrepreneurship Program popularly known as TEF 2023 has started. As an entrepreneur

Read More

As 2023 sets in, it is inheriting the past momentous year of 2022 with is many dramas and events and

Read More

The year 2022 would go down as yet another memorable year with major and significant events. These events included the

Read More

Wema Bank Plc has appointed a new Managing Director to replace Mr. Ademola Adebise who will be commencing his terminal

Read More

As the year comes to an end, it was not without major and outstanding highlights in the football calendar. In

Read More

Cristiano Ronaldo has finally signed for Saudi Arabian Club Al Nassr on a two-year contract. The deal signed this afternoon

Read More

Effective December 31, 2022, all GTBank Naira Mastercard cannot be used for any dollar denominated payments and for any international

Read More

At the close of trading today the All-Share Index increased by 1.89%, representing the month’s largest single-day rise, to close

Read More

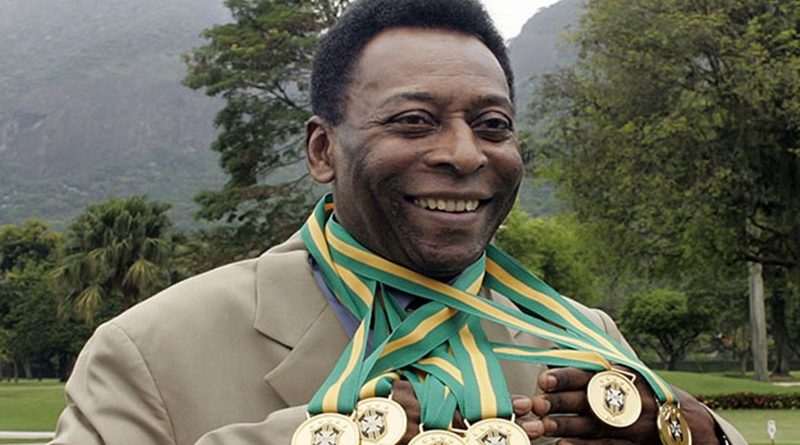

Soccer Legend, Tamar Pele, real name Edson Arantes do Nascimento, is dead. He died yesterday at the Albert Einstein hospital

Read More

The Nigeria stock exchange benchmark index increased by 0.78% to close at 50,300.00 points, which is the highest level since

Read More

The National Assembly yesterday passed into law the 2023 Federal Government of Nigeria budget with a total financial allocation of

Read More

The National Assembly has passed into law the 2023 National appropriation bill or Federal Government budget of N21.82 trillion with

Read More

Ecobank, Nestle, IHS Towers and AstraZeneca have been named among Africa’s Top Best Places to Work for in 2022 The

Read More

According to a press release by the debt management office, as of September 30, 2022, the Federal Government of Nigeria

Read More

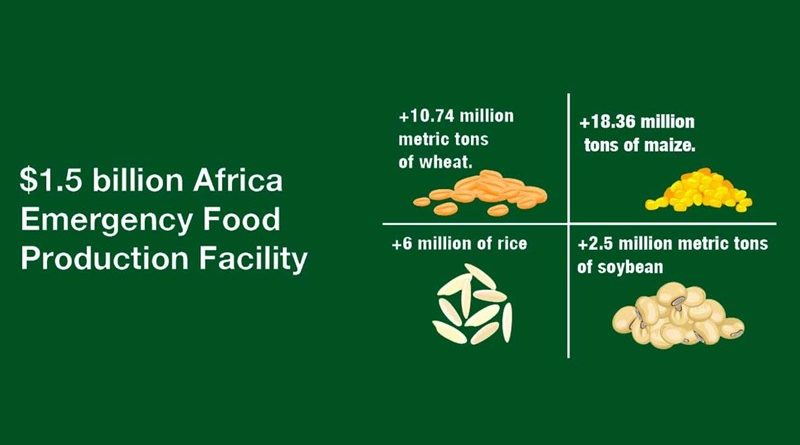

In order to make up for the harm that four Nigerian farmers and their communities claim was brought on by

Read More

The Nigeria stock exchange concluded the week on a strong note by closing the session with the All-Share index up

Read More

A partnership between YouTube and AFRIMA has been formed in advance of the highly anticipated 8th All-Africa Music Awards (AFRIMA)

Read More

The National Assembly is being asked to approve a fresh N819.54 billion extra budget that the Federal Government intends to

Read More

Lionel Messi has agreed in principle to extend his deal with PSG by another year. When he returns from his

Read More

The AKO Caine Prize Award for African Writing is a yearly literary honor given to an African author of a

Read More

Manchester city FC this evening defeated Liverpool FC by three goals to two to advance to the quarterfinals of the

Read More

The Federal Ministry of Communications and Digital Economy has created this skill empowerment program in collaboration with a number of

Read More

Through the “JAMII Femmes” program, Women In Africa and The Coca-Cola Foundation will collaborate in 2022 to support 20,000 African

Read More

One of a kind in Africa, the Qualcomm® Make in Africa Startup Mentorship Initiative will identify promising early-stage startups eager

Read More

The benchmark index of Nigerian Exchanges Limited, NGX All-Share Index, registered a 0.05% rise to close at 49,499.43 points, the

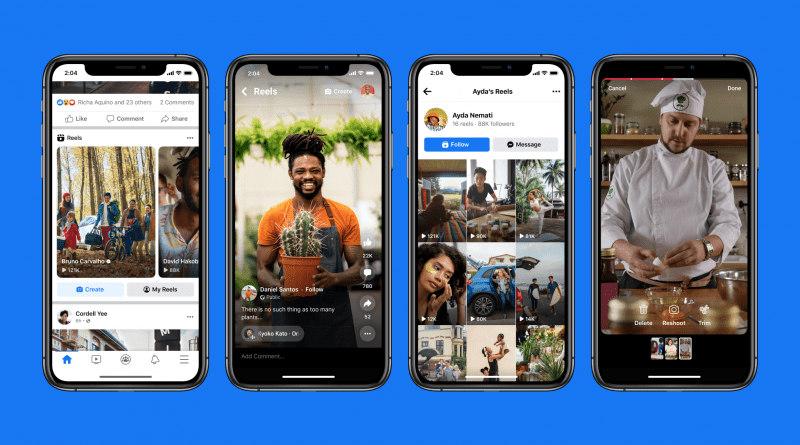

Read MoreMeta today announced its 2022 Africa Year in Review which highlights some of the company’s activities and investments in Sub-Saharan

Read More

On 1st January 2023, The Tony Elumelu Foundation entrepreneurship programme’s application will commence and Entrepreneurs are invited to apply HERE

Read More

Qualcomm, a telecommunications company, announced that it would start a mentorship program for Make in Africa Startups to find promising

Read More

In a circular dated December 21, 2022, title: “Naira Redesign Policy – Revised Cash Withdrawal Limits” and addressed to all

Read More

The benchmark index of the Nigerian Exchange Limited (NGX ASI) rose 0.11% to close at 49,475.43 points on Wednesday, the

Read More

Following several months of intense rain and devastating flooding, the GE Foundation today made a commitment of $100,000 to Nigeria

Read More

The Coalition for Digital Africa is a project started by the Internet Corporation for Assigned Names and Numbers (ICANN) with

Read More

As of December 2022, MTN has amassed an impressive 20 million monthly active users in collaboration with ayoba, Africa’s Super

Read More

AFG (Africa Foresight Group), the tech talent platform with the largest network of independent consultants in Africa, recently hosted a

Read More

In partnership with the Ellen MacArthur Foundation, Parsons School of Design, the United Nations Environment Program, BPCM, and the Centre

Read More

Today, Daughters for Earth announced awards to 26 women-led projects in 17 countries working to preserve and revitalize the planet

Read More

The BNI Foundation has launched a humanitarian effort called Heaters & Hope Initiative to support Children in need in war

Read More

The Rules for Listing on the NGX Technology Board were approved by the Securities and Exchange Commission (SEC) on December

Read More

The benchmark index increased by 0.04% to conclude at 49,416.18 points as the Nigeria Stock Exchange closed higher, extending advances

Read More

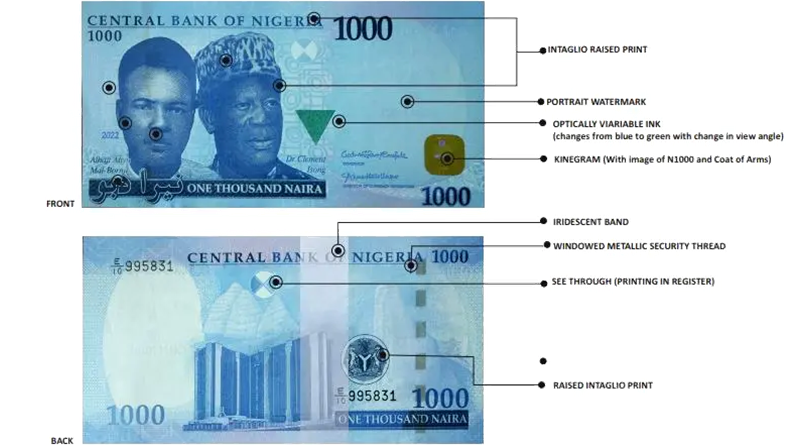

The Central Bank of Nigeria has released the security features of the ne Naira notes which makes counterfeiting difficulty and

Read More

The 2022 CNN Hero of the Year is Kenyan born Nelly Cheboi, who in 2019 left a prestigious software engineering

Read More

The Ukranian President, Volodymyr Zelensky and “the spirit of Ukraine” has been named a Time Magazine’s 2022 Person of the

Read More

Usain Bolt, a Jamaican who has won eight Olympic gold medals, will receive the Lifetime Achievement award at the BBC

Read More

Lionel Messi has been awarded the BBC Sports Personality’s World Sport Star of the Year for 2022.After scoring seven goals

Read More

Tekedia Institute is launching a new course, the Learner Investment Fund and Portfolio Management Program, that will teach students about

Read More

Nigerian stocks began the week on a positive note as the benchmark index closed 0.20% higher than it had the

Read More

The Amazon Web Services (AWS) Healthcare Accelerator 2023 is now accepting applications. The AWS Healthcare Accelerator is a four-week virtual

Read More

For the Global Agrifood Techpreneur Programme 2023, applications are now being accepted. The goal of the global agrifood techpreneur is

Read More

Yes, its very true. Finally Lionel Messi lifts the World Cup for his Country Argentina, he led the La albiceleste (the

Read More

After more than two decades, Angelina Jolie and the UN organization for refugees are no longer working together. The Actor

Read More

The 2022 NGX Made of Africa Awards (NGX MOA Awards) ceremony was successfully organized by Nigerian Exchange Limited (NGX or

Read More

Nigerian Exchange Limited (“NGX” or “The Exchange”) has urged its recently hired brokers to preserve the capital market’s high ethical

Read More

The benchmark index of the Nigeria Stock Exchange (NGX All-Share Index) concluded the week with a 0.17% gain to settle

Read More

The LEDE Fellowship links and supports journalism entrepreneurs with the aim of speeding the spread of solutions journalism and producing

Read MoreThe 8th cohort of the Orange Corners Nigeria Incubation Program is now accepting applications! Orange Corners is a project of

Read More

The Swiss Re Foundation Entrepreneurs for Resilience Award honors business endeavors that use cutting-edge methods to create resilient societies and

Read More

The She Starts Africa Female Founder Program intends to assist you in fostering an entrepreneurial mindset, acquiring the necessary skills,

Read More

Today, Eli Lilly and Company (NYSE: LLY) and EVA Pharma (http://www.EVAPharma.com/) announced their partnership to help at least one million

Read More

IHS Towers, a global provider of communications infrastructure, gave a gift donation to the U.S. Agency for International Development (USAID)

Read More

Due to the disruption of the electricity grid brought on by insecurity, one of Nigeria’s 36 States had been experiencing

Read More

On the sidelines of the 2nd International Conference on Public Health in Africa (CPHIA 2022), which is taking place in

Read More

A new cooperation between Microsoft’s Airband Initiative and Viasat has been revealed in order to provide internet access to ten

Read More

The inflation report for November 2022 as release by the Nigeria Bureau of Statistics shows – Headline inflation rate

Read More

The African Women Impact Fund (AWIF), a partnership between Standard Bank and the United Nations Economic Commission for Africa, has

Read More

Aruwa Capital, a growth equity and early-stage investor, has announced a $2.5 million investment round for Nigerian online retailer Taeillo.

Read More

A pan-African early-stage venture capital firm called Ventures Platform today announced the final closing of its international fund, which totaled

Read More

Jumia has announced the closing of its office in Dubai as it restructures its operations in the wake of years

Read MoreAccess Bank upgraded its IT system, which helped it move up the country’s rankings from 65th to first. A change

Read More

Nigerian stocks continued their upward trend as the benchmark index increased by 0.50% to close at 49,233.02 points, which was

Read MoreThe NGX recovered today, recouping the loss from the previous session as the benchmark Index reached its highest level since

Read More

The hard fighting Atlas Lions of Morocco bowed to defending champions, the Les Bleus (The Blues) of France, 2:0 in

Read More

Argentina today showed class above Croatia as they comfortably beat the European Nation 3:0 in regulation time. With these, the

Read More

Aku zafi? Abdulafar Ahmed made a lighthearted joke while injecting some of the kids at Ruggar Budo, a nomadic hamlet

Read More

Anza Investment Readiness Accelerator Programme Anza provides growth-stage business owners with access to inexpensive, risk-tolerant finance for the rest of

Read More

Today, it was revealed by Coca-Cola Company that Luisa Ortega will take over as president of the organization’s Africa operating

Read More

The NGX All-Share Index closed 0.09% down to settle at 48,853.54 points today, driving the domestic market lower under the

Read More

The majority of grains’ prices on the Exchange and in the open market had a red week. Soybeans were the

Read More

According to the Nigerian Communications Commission the number of active internet users in Nigeria has surpassed the 152 million and

Read More

The Japan-Africa Investment Drive is a funding accelerator that attempts to match high-potential African startups with qualified Japanese Venture Capitals

Read More

A $75 million re-guarantee agreement for Small and Medium Enterprises (SMEs) throughout Africa has been announced by African Guarantee Fund

Read More

The NGX All-Share Index (NGX-ASI) closed 0.04% firmer to conclude at 48,899.08 points on Monday, the highest level since October

Read More

At a recent workshop in Lagos , the FGN together with about 200 stakeholders from various sectors with the assistance

Read More

France beat England on two goals to one to advance to the semi finals of the 2022 World Cup in

Read More

The Atlas Lions of Morocco have beaten the Seleção Portuguesa de Futebol of Portugal in the 2022 World Cup quarterfinal

Read More

Business networkers that are successful understand the need of spending time learning about the value of referral partners’ products or

Read More

Each season, Afrosport will broadcast more than 35 NBA games on free-to-air television in Sub-Saharan Africa; on December 10, the

Read More

The Climate Story Fund encourages captivating storytelling and global impact initiatives that advance a just and biodiverse future. The fund

Read More

The LVMH Prize for Young Fashion Designers was established by LVMH in 2013 and is motivated by a “passion for

Read More

The second of the Flour Mills of Nigeria Plc’s annual Prize for Innovation competition has begun. The objective of FMN’s

Read More

Argentina beat Netherlands 4:3 on penalty kicks to progress to the semi finals of the 2022 World cup in Qatar

Read More

Croatia today secured a well deserved 4-2 penalty win against hard fighting but wasteful Brazil in the first quarterfinals of

Read More

Nigerian stocks staged a comeback in the final trading session of the day, recovering the loss from the previous session

Read More

The AELP Trading Link, a new e-platform created by the African Exchanges Linkage Project (AELP), enables smooth cross-border securities trading

Read More

In honor of this year’s International Human Rights Day, Paradigm Initiative (PIN), a prominent Pan-African human rights and advocacy organization,

Read MoreThe Moove mobility fintech company in Nigeria has raised $30 million to increase its fleet of electric vehicles in the

Read More

The benchmark index for Nigerian equities increased by 0.12% to close at 48,426.49 points, the highest level since October 5,

Read MoreFedEx Express (FedEx) has announced that it has opened a direct commercial presence in Nigeria to fulfill the country’s expanding

Read More

According to data from a Nigerian poll, 33% of IT decision-makers in Nigeria and 34% of them aim to relocate

Read MoreAccess Bank Pic has moved to purchase a 51% majority stake in Finibanco Angola S.A . Finibanco Angola S.A. has

Read More

The Mastercard Foundation Africa Growth Fund’s inaugural investment goes to Aruwa Capital Management, a 20 million USD fund with a

Read More

Purple Real Estate Income Plc (“PREIP” or “Purple”), Nigeria’s ground-breaking real estate investment platform, announced today that the group has

Read More

A joint initiative of the taz Panter Foundation and Reporters Without Borders (RSF), the Rest & Refuge Fellowship. It has

Read More

International journalists who enroll in one of the journalism graduate programs at NYU’s Arthur L. Carter Journalism Institute are supported

Read More

The ambitious Mastercard Foundation Africa Growth Fund, a $200 million Fund of Funds, supports early-stage, growth-oriented small and medium-sized firms

Read More

The FUZE Entertainment Talent Show is open to musicians, dancers, and other individuals with distinctive talents who want a chance

Read More

The Central Bank of Nigeria (CBN) has implemented a daily ATM withdrawal restriction of N20,000 for individual accounts and a

Read More

Portugal easily sent fellow European country packing from the World Cup in the group of 16 match played today. The

Read More

Morocco today sent wasteful Spain out of the World Cup on penalties having played 120 minutes goalless. The teams resorted

Read More

The Nigeria Stock Exchange continued its bull run for a third day in a row, helping the benchmark index gain

Read More

In the open market, paddy rice saw a gain of 8.10%, continuing a two-week streak of gains. Due to its

Read More

The Tony Elumelu Foundation, Africa’s leading and largest entrepreneurship foundation and business catalyst, today released the list of entrepreneurs and

Read More

According to Ifeyinwa Ugochukwu, the CEO of the Tony Elumelu Foundation, TEF has disbursed well over $85m to over 18,000

Read More

The 54th Conference of African Ministers of Finance, Planning, and Economic Development officially opened earlier this year with the launch

Read More

The Nigerian Content Development and Monitoring Board (NCDMB) has started educating 500 Bayelsa State youths on GSM phone technology in

Read More

Brazil, one of the favorites of the 2022 Qatar World Cup tournament lived up to their billing today by defeating

Read More

Croatia today defeated Japan on penalty shootout to advance to the quarterfinals stage of the 2022 World Cup in Qatar.

Read More

The 13 December 2006 adoption of the Convention on the Rights of Persons with Disabilities (CRPD) underlines that all people,

Read More

On Monday the 5th of December, 2022, the NGX All-Share Index (ASI) closed 0.24% stronger to conclude at 48,270.23 points,

Read More

Talented young leaders with a variety of skill sets and backgrounds are sought out by the Global Health Corps (GHC)

Read More

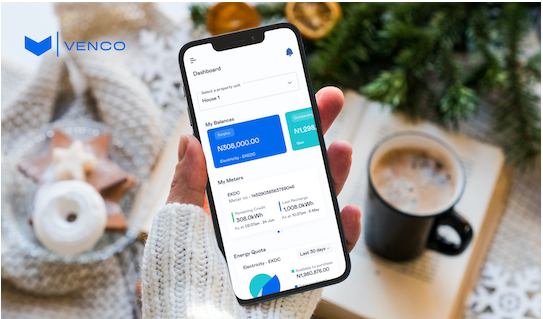

An oversubscribed pre-seed fundraising round netted $670,000 for VENCO, a technology business that offers solutions to improve living conditions in

Read More

Uncover, a skincare company based in Kenya, has reported that it has secured USD $1 million in seed funding, which

Read More

According to The Banker’s Bank of the Year Awards 2022, Zenith Bank Plc has been named Nigeria’s Bank of the

Read More

By exchanging data, including indications of compromise (IoCs) on various cyberthreats and types of cybercriminal behavior targeting African nations, Kaspersky

Read More

Following a number of successful pilot tests using low earth orbit (LEO) satellites in the US and UK, World Mobile

Read More

With a committed $200 million, the Mastercard Foundation Africa Growth Fund (MFAGF), a Fund of Funds, has been established to

Read More

England today defeated the African champions, Senegal, 3-0 in the round of 16 to reach the quarterfinals of the 2022

Read More

In the Round of 16 game, defending champion France defeated Poland 3-1 to advance to the quarterfinals of the 2022 World Cup. Olivier Giroud, a French striker, scored the game’s opening goal in the first half. Giroud surpassed Thierry Henry to become France’s all-time best scorer with 52 goals for his nation. The French lead was increased in the second half by 24-year-old sensation Kylian Mbappé, who scored. Then, during stoppage time, Mbappé made a comeback. For the fifth time in the competition, he scored in the final minute. The youthful sensation is now leading the race for the golden boot with five goals in World Cup 2022. Poland received a penalty in the dying seconds of the match after France was handballed in the box. Robert Lewandowski approached the target. Hugo Lloris stopped the initial attempt, but he was too early off his line. After another attempt, Lewandowski scored to give Poland a consolation. France will now face the winner of the England vs. Senegal

Read More

With his first goal in the World Cup elimination round, Lionel Messi scored in his 1,000th professional match, helping Argentina

Read More

One of the biggest international conferences to confront the situation that even the heads of the plastics industry call a

Read More

Millions of people around the world continue to be impacted by HIV and AIDS, which is a serious public health

Read More

According to the National Bureau of Statistics’ (NBS) most recent national accounts, the GDP increased by 2.3% y/y in Q3

Read More

Uruguay and Ghana have both been eliminated from the 2022 World Cup in Qatar. Giorgian de Arrascaeta scored twice in

Read More

Nigerian stocks completed the week on a high note despite the erratic performance, as the All-Share index closed 1.04% stronger

Read More

The year 2022 is coming to an end in a few weeks, and now is a good moment to take

Read MoreThe 2022 National Sports Festival, tagged “Delta 2022”, #Delta2022, #NSFdelta2022, #NSF, commenced on Wednesday November 30th at the Stephen Keshi

Read More

The 12th Nigeria Aviation Award, along with the customary Cabin Crew Contest for crowning the Nigeria King and Queen of

Read More

Fidet Okhiria, the Managing Director of the Nigeria Railway Corporation has said that all the Abuja – Kaduna train service

Read More

When Group E’s chaotic final two games were played on Thursday, the four-time World Cup champion Germany was eliminated. Germany

Read More

You are cordially invited by Ariana Grande to sample her brand-new fragrance line, MOD, which is a first for the

Read More

The benchmark index of the Nigerian Stock Exchange closed marginally lower by 0.01% to settle at 47,656.64 points as the

Read More

Ahead of the commissioning of the Digital Industrial Park (DIP) project in Kano State Nigeria, the Executive Vice Chairman of

Read More

Alibaba Global Initiatives (“AGI”) today announced the graduation of 86 African entrepreneurs from the latest edition of the Alibaba Netpreneur Training (“ANT”)

Read More

The JA Africa (https://JA-Africa.org/) Company of the Year (COY) Competition, Africa’s largest high school entrepreneurship competition returns for the 12th

Read More

Leading Pan African digital rights and inclusion organization, Paradigm Initiative (PIN) has exclusively premiered its short film christened Finding Diana on the

Read More

UNDP and FCMB have launched the AgroHack Challenge to crowdsource innovative solutions to the challenges faced across the agricultural ecosystem

Read More

The World Bank, with support from the Korea World Bank Partnership Facility (KWPF) and the Korean Green Growth Trust Fund (KGGTF), and in partnership

Read More

DEG Impulse gGmbH and Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH with funds from the German Ministry for Economic Cooperation

Read More

Boomplay (www.Boomplay.com), Africa’s largest music streaming platform, has partnered with Generations Radio, France’s premier syndicated Hip Hop and Soul radio

Read More

NopeaRide, the first fully-electric taxi company that has been in operation since 2018 is folding up its business in Kenya, after failing

Read More

Nigerian food-tech platform Orda announced has raised a $3.4 million seed round to further digitize food businesses across the continent. Orda, which

Read More

The federal government says there is no scarcity of petroleum products and equally no price increases in the commodities at

Read More

The retail price of kerosene in Nigeria has climbed above N1,000 per liter. The poor man’s cooking fuel now sold

Read More

It is 20 years since the last drug for Alzheimer’s was licensed in the UK. Since then, huge advances have

Read More

In the last trading session of the month, Nigerian equities staged a rebound, recouping prior session losses as the benchmark

Read More

The Swedish International Development Cooperation Agency (Sida) has announced a three-year, 66 million Swedish Kronor grant (approximately US $6 million)

Read More

On the 19th of November, 2022, The World’s Leading Cryptocurrency Exchange and Asset Trading Platform, CoinW (http://bit.ly/3gHpB26), organized a VIP Day

Read More

At the recently held Creative Africa Nexus Weekend (CANEX WKND) that brought together the largest gathering for the cultural and

Read More

The Milken Institute and the Motsepe Foundation has launched the Milken-Motsepe Prize in Green Energy, a $2 million prize competition to

Read More

“We were the first African company to lay over 100,000 km of fibre network across the African continent, and we

Read More

Bearish sentiment extended in today’s trading session as the All-Share Index closed 0.24% lower to settle at 47,322.97 points, marking its second successive

Read More

In the open market, Maize and Sorghum sustained a 2-week dip, plunging 3.73% and 0.02% respectively. This was attributed to

Read MoreSterling Bank Plc, Nigeria’s leading commercial bank, has partnered with Nigeria Jubilee Fellows Programme (NJFP) to sponsor 1,000 fellows during

Read More

The 6th World Circular Economy Forum WCEF2022 (www.WCEF2022.com) will take place 6–8 December in Kigali, Rwanda. This year’s forum will

Read More

Three years of flatlined progress on HIV treatment and prevention affect 2.7 million youth . Some 110,00 youth under age

Read More

APO Group (www.APO-opa.com), the leading Pan-African communications consultancy and press release distribution service, today announced a content agreement with Pan-African

Read More

Liquid Intelligent Technologies (https://www.Liquid.Tech/), a business of Cassava Technologies, a pan-African technology group, officially announces the launch of its operations

Read More

Starting the week, the Lagos bourse halted its six-day winning streak as the All-Share Index lost 0.25% to settle at 47,436.45

Read More

Daily, new, and experienced investors routinely ask us questions such as “Why is understanding the commodities market so complicated?” “Why can’t

Read More

Tekedia Institute is very excited to invite the general public to Tekedia Mini-MBA edition 9 graduation lecture on Saturday, Dec

Read More

Paradise Game (ParadiseGame.net), beacon for esports and edtech in Africa, initiated with VISA, a regional program to promote financial education

Read More

Last week, Meta (www.Facebook.com) invited top Nigerian content creators to a first-of-its-kind mixed reality event showcasing creativity and imagination as keys to

Read More

In September, blockchain platform Polygon opened applications for its Web3 Bootcamp targeting African developers. The Polygon Bootcamp and Hackathon was the company’s

Read More

The UNICEF Venture Fund is looking to make up to US$100K in equity-free investments to provide early-stage (seed) funding to

Read More

Innovate Now has helped to launch 21 African assistive tech ventures over four acceleration cycles. African start-ups receive mentorship, learning

Read More

The CGIAR Food Systems Accelerator aims to support agribusinesses in scaling their climate-smart innovations. These innovations are aimed at agrifood

Read More

The UN Global Compact Business & Human Rights Accelerator is a six-month programme activating companies participating in the UN Global

Read More

Nigerian fintech startup, Pivo, has closed a $2 million seed round that included participation from Precursor Ventures, Vested World, Y

Read More

Ending the perfect week, Nigerian equities closed the session stronger, bringing the All-Share index up by 2.04% to settle at 47,554.34

Read More

In response to the discovery of a new attack that compromises victims’ VPN (Virtual Private Network) accounts to compromise messaging

Read More

Business Council for Africa announces launch of Africa’s first business book awards. Total prize money of $17,500 to be awarded

Read More

Unity Bank Entrepreneurship Development Initiative – Corpreneurship Challenge, targeted at empowering fresh graduates and Corp Members on one-year compulsory national youth service

Read More

With the global population recently reaching 8 billion, we can celebrate many signs of human progress. Better health and longer

Read More

MMV (http://www.MMV.org) and Shin Poong Pharm. Co., Ltd. welcome the formal inclusion of Pyramax® (pyronaridine-artesunate) in the World Health Organization’s (WHO) Guidelines

Read More

Africa Data Centres, a business of Cassava Technologies, a pan-African technology group, is proud to be the colocation provider for

Read More

On November 22, U.S. Consul General Will Stevens and the Lagos State Governor Babajide Sanwo-Olu held a handover ceremony to

Read More

Extending gains for the fifth consecutive session, the Lagos bourse closed higher as the benchmark index gained 0.81% to settle at 46,604.94

Read More

The national accounts for Q3 ‘22 by the NBS show that GDP grew by 2.3% y/y compared with the 3.5%

Read More

CarbonAi Inc., CarbonAi, has signed a memorandum of understanding (MOU) with the Rural Electrification Agency (REA) of Nigeria to identify

Read More

Partner2Connect is an international digital alliance that aims to deliver digital connectivity to more than 80 countries by 2025. It

Read More

Autochek, the automotive technology startup making car ownership more accessible and affordable across Africa, has announced the launch of Autochek

Read More

Ramani, the African software company building a cloud network of micro-distribution centres for Africa’s $1 Trillion consumer-packaged goods supply chain,

Read More

Flapmax (www.Flapmax.com) announced today the launch of AI Builders Garage, a global on- and offline platform designed to help young entrepreneurs

Read More

For the fourth consecutive session, the Nigerian Stock Exchange maintained the winning streak as the benchmark index closed 2.90% stronger – the

Read More

Following the success of the MultiChoice (www.MultiChoice.com) Africa Accelerator (https://bit.ly/3OtthRz) Programme, which secured $16 million (USD) of funding for six emerging

Read More

President Muhammadu Buhari unveiled the newly redesigned N200, N500 and N1,000 banknotes at the presidential villa today. The newly redesigned

Read MoreFinancial Solutions for Migrants is an accelerator for impact-driven startups developing bold solutions that increase the financial inclusion of migrants,

Read More

The Making More Health Business Accelerator, is a structured business growth program targeted at social entrepreneurs with innovative solutions in the

Read More

JFD is calling on women from Europe and Africa, engaged in bold technological bets that create disruptive innovations to change

Read More

Deutsche Welle (DW) is looking for young people from all over the world interested in a comprehensive, exceptional quality journalism

Read More

The Jim Leech Mastercard Foundation Fellowship on Entrepreneurship gives African students and recent graduates the opportunity to access training, resources,

Read More

The U.S. Trade and Development Agency (USTDA) announced it has awarded a grant to Fly Zipline Ghana, for a feasibility study to

Read More

Two African startups, BleagLee and LiquidGold in addition to Ryp Labs, Earthly, Koltiva have been announced as winners of the

Read More

It was a buyer’s market in the open market last week. Prices plunged across grains commodities with Soybean topping the

Read More

For the third consecutive session, the Lagos bourse maintained the bull run bringing the benchmark index up by 0.60% to

Read More

Eleven (11) members of the monetary policy committee of the CBN were in attendance. Decision The eleven members

Read More

The African Management Institute (AMI) (www.AfricanManagers.org), the continent’s leading business learning company has announced the launch of AMI Enterprise (https://bit.ly/3UVXTNR),

Read More

The African Union Commission (AUC) and the African Development Bank have signed a grant agreement to implement Phase 1 of the

Read More

African AI and blockchain startups are set to benefit from Modus Africa fund, an African –focused venture capital firm under

Read More

Macroeconomic and fiscal reforms are urgently needed to lift Nigeria’s development outcomes, which are severely constrained by inefficient use of

Read More

Nigerian equities opened the week strong today as the benchmark index gained 0.47% to close at 44,701.84 points, the highest point since

Read More

The Africa’s Business Heroes (ABH) Prize Competition (www.AfricaBusinessHeroes.org), a philanthropic initiative sponsored by the Jack Ma Foundation and Alibaba Philanthropy, announced

Read MoreNigeria Sales Conference is a nonprofit initiative of The Selling Champion Consulting Limited, a Nigerian Council For Management Development accredited

Read More

Developing countries celebrated on Sunday morning as crucial climate talks ended with a “historic” deal on their most cherished climate goal: a

Read More

In the last trading session of the week, the domestic bourse ended the week on a positive note as the All-Share

Read More

The DMO held its monthly auction of FGN bonds on Monday (14 November ’22). It offered N225bn (USD503.7m) but raised

Read More

Qrios, the Digital Economy Empowerment Platform has built a utility for commerce. It is designed from the ground up to

Read More

Hard Rock Cafe is expanding upon its partnership with world-renowned soccer legend Lionel Messi with its latest release of its fan-favorite Messi

Read More

The African Exchanges Linkage Project (AELP), has gone live on integrating the African capital markets by facilitating cross-border trading and

Read More

Finland is set to be one of the first countries to develop a fully circular plastics economy by 2030. Led

Read MoreApplications for H&M Foundation’s Global Change Award 2023 are now open. This is an innovation challenge that aims to find,

Read More

Elon Musk issued an ultimatum on Wednesday, and as a result, Twitter offices are closing and staff members are quitting

Read More

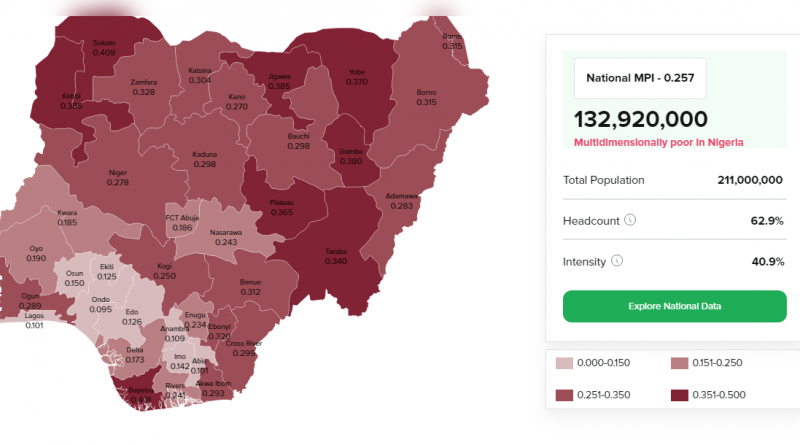

The Federal Government of Nigeria through the National Bureau of Statistics today launched the results of the 2022 Multidimensional Poverty

Read More

Today, the bears dominated the domestic bourse as the NGX All-Share Index (ASI) fell by 0.09% to settle at 44,011.22 points. The

Read More

Financial Solutions for Migrants is an accelerator for impact-driven startups developing bold solutions that increase the financial inclusion of migrants,

Read More

The Making More Health Business Accelerator, is a structured business growth program targeted at social entrepreneurs with innovative solutions in the

Read More

Through the Responsible Computer Science Challenge, USAID and Mozilla are supporting the conceptualization, piloting, and scaling of curricula that integrate

Read More

JFD is calling on women from Europe and Africa, engaged in bold technological bets that create disruptive innovations to change

Read More

Our current food system is at the heart of many of today’s biggest opportunities and challenges. It’s clear that we

Read More

The African Development Bank (www.AfDB.org) and the West African Monetary Union’s Capital Markets Authority (AMF-UMOA) have signed a grant agreement

Read More

City rankings by the number of Unicorns, Exits, Pantheons, and Influencers; Most Recent Industry Reports; Somalia’s startup ecosystem; CrunchBase Exclusive

Read More

The FIFA World Cup Qatar 2022™ is the most awaited sports event of 2022 for football fans and kicks off

Read More

Cape Town, South Africa, November 17th, 2022 – AFG (Africa Foresight Group), the tech talent platform with the largest network

Read More

The Board of Directors of the African Development Bank Group has approved an equity investment of $20 million in Evolution

Read More

Paystack has joined a number of other providers that have been granted payments license to operate in Kenya. The company

Read More

It’s now emerging that the collapse of American crypto platform FTX last week has had an impact on Nigeria’s Web3 startup Nestcoin,

Read More

In continuation of its operations improvement and power plant modernization plan, Indorama Eleme Petrochemicals Limited (IEPL) and GE Gas Power

Read More

Pan-African housing development financier Shelter Afrique has approved a USD13 million line of credit to Lagos-based real estate firm, Mixta

Read More

Nigerian equities recovered as the benchmark Index rose by 0.55% to settle at 44,050.44 points. Bullish sentiment in telco heavyweights, MTNN

Read More

Nigeria’s leading commodities market player, AFEX, has unveiled its 2022 Wet Season Crop Production Report in a hybrid event hosted

Read More

The THRIVE | Shell Climate-Smart Agriculture Challenge aims to identify and support top start-up and scale-up innovators who are driving

Read More

Graduates of the 10,000 Women online course at Goldman Sachs can now apply for the 10,000 Women Growth Fellowship. The

Read More

Global AgriInno Challenge, a worldwide competition for youth agripreneurs and innovators, showcases and promotes smart digital innovative talent. With the last

Read More

IFC announced the appointment of Sarvesh Suri as the new Regional Industry Director for Infrastructure and Natural Resources in Africa. Suri, who

Read More

Enough is Enough Nigeria, BudgIT Foundation and Paradigm Initiative are set to host the fifth edition of the New Media,

Read More

Activity on the Lagos bourse was mixed albeit with a bearish tilt as the benchmark index closed marginally lower by

Read More

UTM Offshore will sign an agreement for the Front-End Engineering Design (FEED) for Nigeria’s first Floating Liquefied Natural Gas (FLNG)

Read More

The NBS has released its October inflation report to show – Headline rate 21.09% y/y (20.77% in September);Core rate 17.76% y/y

Read More

PalmPay (www.PalmPay.com), a fintech innovator aiming to make digital payment more accessible and flexible, has obtained a compliance status on

Read More

Leading international icons open video campaign; football’s unifying power to be highlighted on global stage at FIFA World Cup; President

Read More

The global population is projected to reach 8 billion on 15 November 2022, signalling major improvements in public health that

Read More

In a review of last week’s performance, Maize and Paddy rice appreciated marginally by 0.06% and 0.32% respectively on the

Read More

Internet users in Africa will soon have faster access to services on the Internet and better protection from cyberattacks. The Internet Corporation

Read More

Britain’s stock market has lost its position as Europe’s most-valued, with France taking the top spot, data shows. A weak

Read More

The Lab is looking for innovative finance solutions that can unlock investment to tackle some of the most difficult climate

Read More

The Emerging Markets Climate Action Fund invests $25 million and EIB (www.EIB.org) Global invests $75 million in Alcazar Energy Partners II; The

Read More

The framework supports environmental investments across the world, thus contributing to green, resilient and equitable development.The EIB (www.EIB.org) is enhancing the

Read More

World Diabetes Day is a global occasion on which people with diabetes, health professionals, diabetes advocates, media, the general public

Read More

Nigerian equities opened the week on a negative note, as the All-Share Index declined by 0.30% to close at 43,837.89

Read More

Every season, trends influence the production and output volumes of commodities in our food systems. This makes it pertinent to

Read More

Making More Health Accelerator 2023 The accelerator offers opportunities for healthcare innovations access to technical and financial support, and mentorship.

Read More

Only 46% of people living with diabetes in the African region know their status, raising the risk of severe illness

Read More

In a bid to promote SDG 8 for decent work and economic growth, Nigerian lender, Unity Bank Plc is collaborating with Kitian Training Hub,

Read More

Three Nigerian fintech startups DT2 Technologies, Bunce and ShipBubble are among the nine African startups selected for the €7.5 million Startup Wise

Read More

Banks, financial services providers, and telecommunication companies from 12 African countries lost $11 million to hacking attacks between 2018 and

Read More

Pan-African housing development financier Shelter Afrique has approved a USD13 million line of credit to Lagos-based real estate firm, Mixta

Read More

The British Council in collaboration with Microsoft has launched a new programme to help young African entrepreneurs in the creative

Read More

Reporters Without Borders Germany is calling for applications for its Berlin Scholarship Program: Empowering Journalists in the Digital Field. From

Read More

The Women Techsters Bootcamp strives to provide adequate learning opportunities for participants to develop relevant coding skills, jump-start careers, or

Read More

TechBridge is a technology Incubator and Accelerator that supports tech-venture founders through the hurdles of early-stage innovation and business development.

Read More

The Roux Prize was created to honor individuals or groups from around the world who have used health evidence in

Read More

The Aurora Tech Award is an annual prize for women founders of IT startups whose projects have had the most profound impact on world development.

Read More

Social impact investor and worldwide cooperative Oikocredit is providing a three-year term loan of $1 million to Standard Life Organisation,

Read More

Eutelsat Communications, the satellite operator has inked a deal with Tizeti, West Africa’s pioneer solar-based internet service provider and a

Read More

Twenty African youth-led enterprises have won grant funding of up to $100,000 each in this year’s African Youth Adaptation Solutions

Read More

Africa must invest in Science, technology, engineering, and mathematics (STEM) education for women and girls, disciplines which would boost their

Read More

Plans to introduce new age fintech solutions around digital lending in the country; Will help banks to launch new and

Read MoreIn line with its strategic intent to always provide solutions and business support for its customers, leading financial institution, Fidelity

Read More

The gross monthly distribution by the Federation Account Allocation Committee (FAAC) to the three tiers of government and public agencies

Read More

Extending gains for the third consecutive session, the domestic bourse ended positive, as the ASI gained 6bps to settle at

Read More

VFD Group has released its unaudited financial statements for the period ended 30th September 2022 (Q3 2022). The Group’s result shows

Read More

In this interview, the Business Director/Chief Operating Officer of Fonbol Energy Services, Mr. Idris Fonahanmi, shares the vision and activities

Read More

Stakeholders in the Nigerian clean cooking space have agreed to work together to accelerate the transition to sustainable clean cooking

Read More

The bears continued to dominate the Lagos bourse as the benchmark index gave up 0.21% to close at 43,745.73 points,

Read More

Stock Rating: BUYPrice Target: N328.65Price (28-Oct–2022): N220.50Potential Upside / Downside: +49.1%Tickers: DANGCEM NL / DANGCEM.LG Dangote Cement (DANGCEM) released its Q3 22 unaudited results after

Read More

Stock Rating: SELLPrice Target: N44.60Price (28-Oct–2022): N70.00Potential Upside / Downside: -36.28%Tickers: BUACEMEN.NL / BUACEMENT.LG BUA Cement (BUACEMENT) released its 9M 22 unaudited results after trading

Read More

Last week, most grain commodities closed in the green territory, returning gains to investors on the Exchange. Paddy rice led

Read More

High Opex drags on Q3 22 earnings despite low finance costs and pioneer incentives. Stock Rating: BUYPrice Target: N39.23Price (01-Nov–2022): N22.25Potential Upside /

Read More

The Women’s Leadership Accelerator is a yearlong intensive program that supercharges the leadership and management skills of women who are

Read More

Retail lender, Unity Bank Plc has declared a N2.2 billion profit for the nine-month period ended September 30, 2022, with

Read More

Ending the week, the Lagos bourse extended its two-day bear run as the benchmark index closed 1.64% weaker – offsetting early week gains –

Read More

Ecobank Group (www.Ecobank.com) is proud to announce that Touch and Pay a Nigeria-based fintech has won the 2022 edition of

Read More

Tesla CEO Elon Musk has closed a deal to acquire Twitter, ending a monthslong saga that cast Musk as suitor,

Read MoreThe European Investment Bank (EIB) has agreed to €100 million financing with MTN Nigeria to support the telecommunications company’s network expansion

Read More

La Fabrique Cinéma has been created by the Institut français, in partnership with France Médias Monde, the SACEM (French society

Read More

Applications are now open for the SDG Innovation Accelerator for Young Professionals, an opportunity for participating companies of the UN

Read More

The AWS Startup Loft Accelerator is an equity-free program focused on supporting early stage startups in Europe, Middle East and

Read More

Applications are now open for the 28th BBC World Service International Radio Playwriting Competition. The global competition, hosted by BBC

Read More

You are invited to submit proposals for scalable and sustainable applications that can serve as a reference point for the

Read More

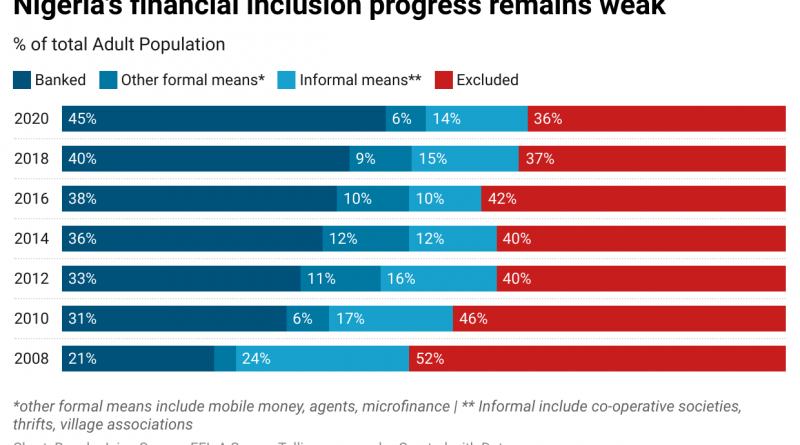

Ghana has been recognized as the only country in Africa to achieve 100% access to financial inclusion on the continent.

Read More

The Central Bank of Nigeria has made the Naira makeover announcement. At a news conference in Abuja, the CBN Governor,

Read More

Today, the NGX All-Share Index relapsed by 0.52% to close at 44,625.18 points – halting five days of successive rally on

Read More

The third straight rate hike this year was announced by the European Central Bank on Thursday along with a reduction

Read More

Sterling Bank Plc, Nigeria’s leading commercial bank, has said there are massive opportunities in the agricultural sector of the Nigerian

Read More

MTN Group has announced that the network will host an Africa-first virtual concert in Ubuntuland, Africa’s metaverse. In February this

Read More

FSD Africa announced the appointment of Arunma Oteh, a seasoned business leader, to the Board of Directors to support the organisation’s

Read More

Online shopping has become an increasingly popular way to purchase things, but delivery fees remain a concern for many consumers.

Read More

Plastic recycling has turned out to be a “failed concept” used by global corporations as a “smokescreen,” Greenpeace USA has

Read More

Today, Nigerian equities extended gains for the fourth consecutive session as the All-Share index gained 0.73% to close at 44,788.14 points.

Read More

Apple outlined what apps can do with cryptocurrencies and non-fungible tokens (NFTs) in a clarification of its policies around these

Read More

Adidas cut ties with Ye, formerly known as Kanye West, on Tuesday following the musician’s harsh and antisemitic (antiJewish) remarks.

Read More

The Mastercard virtual payment solution, linked to Cellulant’s payment gateway – Tingg, can unlock a host of opportunities for consumers,

Read More

Nigeria on Monday began its long journey to end hunger and achieve food security by launching the Special Agro-industrial Processing

Read More

Andela, the global marketplace for remote technical talent, has opened applications for its upcoming EPIC Tournament. In partnership with HackerEarth,

Read More

Nigerian social commerce startup, Bumpa, raises $4 million seed round led by Base10 Partners, the largest black-led fund in the

Read More

Shelter Afrique is developing a Sovereign Lending product to supplement its traditional products that attend to both the demand and

Read More

Opening the week, Nigerian equities extended its winning streak as the benchmark index closed 0.15% stronger to settle at 44,461.43 points.

Read More

Spotify has announced a first-of-its-kind podcast initiative on the continent, the Africa Podcast Fund, with the goal of supporting podcasters

Read More

The President of Nigeria, Muhammadu Buhari, jointly with the African Development Bank, the Islamic Development Bank and the International Fund

Read More

The latest data released by the Nigerian Communications Commission (NCC), the industry regulator, show that internet subscriptions stood at 152.3

Read More

The African Development Bank (www.AfDB.org) has launched a multinational project to create jobs and improve livelihoods for youth in three

Read More

The U.S. Trade and Development Agency (USTDA) announced it has awarded a grant to Nigeria’s Mobihealthcare (Mobihealth) for a feasibility

Read More

In the last trading session of the week, the NGX All-Share Index settled 0.15% higher at 44,396.73 points. Gains in BUACEMENT (+1.64%),

Read More

Polaris Bank is pleased to announce that it has been notified of the completion of a Share Purchase Agreement (SPA)

Read More

Sub-Saharan Africa faces one of the most challenging economic environments in years, marked by a slow recovery from the pandemic, rising

Read More

Activity on the Lagos bourse was mixed, albeit with a bullish tilt as the benchmark index closed marginally higher (+0.03%)

Read More

TSL is partnering with ZooLab for 2022 International Sustainability Challenge Video competition ‘My Local Sustainability Challenges’ Sustainability is a global issue,

Read More

Applications are open for the Adaptation Fund Climate Innovation Accelerator (AFCIA) administered by the United Nations Development Programme (UNDP). The

Read More

Since 1973, journalists have competed for prestigious Kiplinger Fellowships. In recent years, hundreds of journalists from around the world have applied annually

Read More

The African Development Bank Group’s Affirmative Finance Action for Women in Africa (AFAWA) initiative is launching its second call for

Read More

Nigeria has become the latest country to pass a Startup Bill, giving a more formal approach to how the startup

Read More

LHoFT has announced the 15 fintech startups that have been selected to participate in the fifth edition of the CATAPULT: Inclusion

Read More

A record 29 cities across Africa and beyond will play host in November to a physical gathering of investors, in

Read More

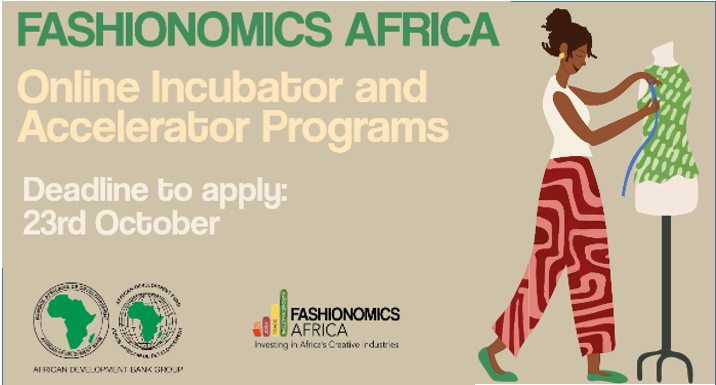

The African Development Bank (AFDB) is working with Co-Creation Hub, The Creative Economy Practice at CcHUB and Syndicate by CcHUB to execute the AFDB Fashionomics Accelerator programme that will

Read More

Mastercard has introduced a new program to enable financial institutions to bring secure crypto trading capabilities and services to their

Read More

Nigeria and Cameroon have expressed interest in joining the alliance for economic relations on cocoa between Côte d’Ivoire and Ghana;

Read More

Moove, the world’s first mobility fintech and Uber’s largest vehicle supply partner in EMEA, is announcing it has raised £15

Read More

In its third session of week, the benchmark index slid further by 2.31% to settle at 44,318.15 points – the lowest point

Read More

The IMF’s World Economic Outlook released last week forecasts that global economic growth will slow from 3.2 percent this year to 2.7

Read More

Union Bank of Nigeria “Union Bank” has announced the first banking partnership with globally recognised telehealth services company Mobihealth International

Read More

Data from the Central Bank of Nigeria (CBN) shows that Nigeria’s external reserves dropped to $37.9 billion as of Wednesday,

Read More

In September 2022, Nigeria’s daily crude oil production, as shown in the monthly oil market report (MOMR) of the Organization of the

Read More

In the October edition of the World Economic Outlook, the International Monetary Fund (IMF) retained its 2022 global economic growth projection at

Read More

Amni International Petroleum Development Company Limited, a Nigerian independent oil and gas exploration and production company and the African Export–Import

Read More

The last trading week saw an increase in the open market price of most grains. Sorghum, Maize, Wheat, and Paddy

Read More

TECNO (www.TECNO-Mobile.com), the global premium smartphone and smart device brand, today launched its brand-new SPARK 9 Pro Sport Edition for

Read More

The MultiChoice (www.MultiChoice.com) Talent Factory (MTF) Academy held its annual graduation ceremonies in October this year. The graduations celebrated the

Read More

Nigerian equities opened the week sharply lower, eroding prior week gains as the All-Share Index lost 2.52% to settle at 46,368.65 points

Read MoreFidelity Bank plc (“Fidelity Bank” or the “Bank”) announced today the redemption of the $400,000,000.00 Eurobond Notes due October 17,

Read More

The NBS has released its September inflation report to show – Headline rate 20.77% y/y (20.52% in August);Core rate 17.60%

Read More

AFEX, Africa’s leading private commodities market player, on Friday, marked World Food Day 2022, with the launch of a new

Read More

Kaspersky researchers discovered a new malicious version of a popular WhatsApp messenger mod dubbed YoWhatsApp. Popular for having features that

Read More

Treten Networks, an ICT solutions and Enterprise security services business, has partnered with Africa Data Centres to allow customers access to the

Read More

As political campaigns begin ahead of the 2023 general elections, the Lagos State Signage and Advertisements Agency (LASAA) has promised

Read More

The IMF’s latest World Economic Outlook (WEO) has left its global forecast for 2022 unchanged at 3.2% y/y and has

Read More

In the last trading session of the week, the domestic bourse recovered as the All-Share Index gained 0.09% to settle at

Read More

The African Development Bank (AfDB) is working with Co-Creation Hub, The Creative Economy Practice at CcHUB, and Syndicate by CcHUB

Read More

An estimated 670 million people are projected to be undernourished in 2030, as noted in FAO’s The State of Food

Read More

Nokia has today announced the launch of a marketplace for broadband network automation applications. Seven apps are available at launch,

Read More

Some of Africa’s newest business success stores are gaming start-ups. Much of Africa’s economy is stable and the gaming culture

Read More

The creative economy offers a feasible development option to all countries, particularly developing economies, says UNCTAD’s Creative Economy Outlook 2022. UNCTAD defines

Read More

Skills and competencies of quantity surveyors have been identified as critical to cost management and local content expansion in Nigeria’s

Read More

Activity on the Lagos bourse was mixed albeit with a bearish tilt as the benchmark index closed marginally lower by 0.02% to

Read More

The six finalists were chosen following extremely strong competition from over 700 fintechs from 59 countries; Grand Finale to be

Read More

Google cloud users will now be able to pay for their services using crypto. This is after Google partnered with

Read More

Lowering trade finance costs could provide billions in economic benefits in four West African countries, according to a new report

Read More

MEST Africa has announced the 36 technology startups from 5 African countries that have been selected for the regional pitch

Read More

MultiChoice has announced its media broadcast partnership with The Earthshot Prize to help accelerate and spotlight the ingenuity and ambition

Read More

Nigerian health-tech startup Lifestores Healthcare has raised $3M for expansion across the country in a pre-Series A funding round. The

Read More

Dooka has partnered with Tradeshift, the global network for digital trade, to launch the first-ever pan-African digital marketplace for business-to-business

Read More

The urban population of Nigeria constituted 48% of the country’s population, according to the United Nations. This indicates that 73.92

Read More

Nigerian data and intelligence company, Stears has raised $3.3 million to enhance its data collection and analytics capabilities, acquire talent

Read More

Today, the domestic bourse slipped as the benchmark index closed 0.07% weaker at 47,531.84 points. Gains in ZENITHBANK (+0.26%) were

Read More

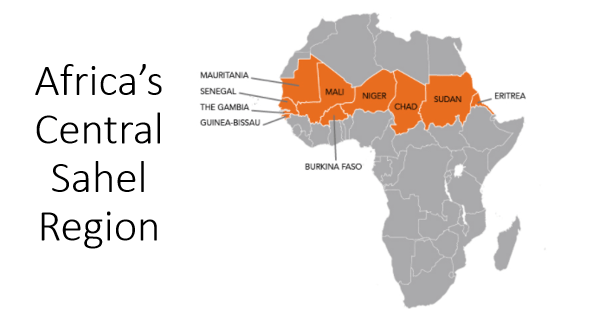

West Africa and the Sahel are experiencing a continuous deterioration of food and nutritional conditions as a result of the

Read More

TLcom Capital, the Africa-focused venture capital firm, has officially announced the launch of its fourth annual Africa Tech Female Founder

Read More

The first cargo of vegetable oil for biorefining produced by Eni in Kenya has left the port of Mombasa, on

Read More

Globacom, the telecom industry transformational leader, has announced the commencement of its payment service bank business with the official launch

Read More

The ECOWAS Commission through the Organised Crime: West African Response on Cybersecurity and Fight against Cybercrime (OCWAR-C,) project funded by

Read MoreThe Alibaba Netpreneur Training program will bring digital entrepreneurs and business leaders together to explore how to harness digital technology

Read More

Alibaba Global Initiatives (AGI), a professional training arm of Alibaba Group (https://www.AlibabaGroup.com/), today enrolled the second class of more than

Read More

Syngenta Crop Protection is launching a commercial digital solution to diagnose infestations of plant-parasitic nematodes in crops by analysing photographs

Read More

The 2023 Hult Prize Challenge is now open for applications to create a for-profit social venture in the fashion/clothing industry.

Read More

Catholic Relief Services’ International Development Fellows Program prepares dedicated global citizens to pursue a career in international relief & development

Read More

Vella had initially launched to provide a platform that powers crypto infrastructure and spending ability in Africa. With this iteration, the

Read More

The gauge for world food commodity prices declined for the sixth month in a row in September, with sharp drops

Read More

The World mental health day 2022, #WorldMentalHealthDay, will be celebrated today Monday October 10th with the theme: Make mental health

Read More

Retail lender, Unity Bank Plc has received an Award of Recognition for emerging as the “Best Bank in Customer Complaint

Read More

Sterling Bank Plc has announced plans with her partners Leadway Assurance, Nestle Nigeria Plc, Microsoft Nigeria, Thrive Agric, GIZ, Stears

Read More

Over the past 18 months, the headline inflation has recorded upticks on a y/y basis. The headline inflation is currently

Read More

Like many health workers across the Sahel, Mairama Baba Yadafa has been witnessing first-hand the multiple impacts of an unprecedented

Read More

The Japanese Award for Most Innovative Development Project is a competitive grant program under the umbrella of the Global Development Awards

Read More

CFYE aims to co-invest in innovative, private sector-led partnerships that aim to address the youth unemployment challenge by creating, matching, and improving jobs for

Read More

APO Group (www.APO-opa.com), the leading Pan-African communications consultancy and press release distribution service, today announced that Daniel Adeyemi from Nigeria

Read More

In today’s session, Nigerian equities ended their three-day losing streak, as the All-Share Index (ASI) closed 0.19% higher at 47,351.43 points.

Read More

The AFRIFF (Africa International Film Festival), announced its 11th edition holding between the 6th and 12th of November 2022. Speaking

Read More

NESCAFÉ, Nestlé’s largest coffee brand and one of the world’s favorite coffees, outlined today its extensive plan to help make

Read More

Local efforts in Nigeria to increase the pace of digitalization and ensure regulatory compliance are being ramped up across industry

Read MoreMeta today unveiled an exclusive XR exhibition featuring the six finalists from the ‘Future Africa: Telling Stories, Building Worlds’ programme, focused on supporting

Read More

The incidence of floods across 29 of 36 states in Nigeria casts more worries for Nigeria’s food security in the

Read More

Pan-African phone manufacturer Mara Group has launched a free educational online course with the aim to boost blockchain adoption and

Read More

According to Kaspersky’s Financial Cyberthreats report, attacks in the financial sector are becoming increasingly corporate-oriented and shifting away from consumers. Kaspersky Security

Read More

Agriculture remains integral for developing economies, capable of stimulating growth across the non-oil economy via its broad potential value-chain interlinkages.

Read More

The winners of the 2022 AWIEF (www.AWIEForum.org) Awards were announced on Tuesday at a glittering ceremony on the rooftop of The

Read More

As part of our efforts to educate and inform on different domains of market system and business, Tekedia Institute is partnering with

Read More

In the last trading session of the week, the domestic bourse recovered as the All-Share Index gained 0.12% to close

Read More

In a 2019 vector alert, WHO identified the spread of Anopheles stephensi as a significant threat to malaria control and elimination – particularly

Read More

In a massive collaborative initiative to support and promote interventions targetted to addressing hunger and malnutrition in communities, Agric lender, Unity Bank Plc and Lagos Food Bank

Read More

Experts at the WTO Public Forum deliberate on greening micro, small and medium-sized enterprises to harness the benefits of the

Read More

In August, WHO’s Monitoring Report on Universal Health Coverage in Africa revealed a 10-year rise in life expectancy between 2000

Read More

The domestic bourse ended the session mixed albeit with a bullish tilt as the benchmark Index managed to eke out

Read More

Applications are open for Polygon Bootcamp Africa, launched in partnership with Xend Finance! The eight-week intensive educational course and hackathon combo

Read More

The New Media Writing Prize (NMWP) encourages and promotes the best in new-media writing and is leading the way toward

Read MoreThe 2023 Accountability Incubator is looking for the very best ideas from young people for accountability, participation and open government.

Read More

The THRIVE | Shell Climate-Smart Agriculture Challenge aims to identify and support top start-up and scale-up innovators who are driving

Read More

Ericsson and MTN Nigeria have reached a milestone with the successful launch of 5G services. This deal is the result

Read More

OmniBiz, a platform digitizing the essential goods ecosystem has announced a brand refresh. The refresh reaffirms OmniBiz’s commitment to digitizing

Read More

Kowry Energy, a sustainability-driven energy service provider focused on power provision across Sub-Saharan Africa, announced the successful commissioning of four

Read More

Decision The twelve members unanimously voted to raise the MPR.• Ten out of twelve members voted to raise MPR by 150bps to

Read More

SecondSTAX (Secondary Securities Trading and Aggregation eXchange) of Ghana, announced it has raised $1.6 million in pre-seed funding from private investors

Read MoreGhanaian agritech startup Farmerline announced the second close of a Pre-Series A investment raise with an additional $1.5 million investment

Read More

Proparco announced a $20 million Trade Finance Guarantee Facility for Coronation Merchant Bank (CMB), to establish and deepen partnerships with

Read More

The domestic bourse ended lower today reversing some of the gains of yesterday’s session as the benchmark index lost 0.11%

Read More

As the malnutrition crisis in northwest Nigeria continues at catastrophic levels, Médecins Sans Frontières (MSF) is calling for the international

Read More

Says Tiekie Barnard, Shared Value Africa Initiative (SVAI) CEO and Founder: “We are co-creating the global future on the African

Read More

As part of Union Bank’s commitment to driving financial inclusion in Nigeria, the Bank has partnered with WACOT Rice Limited

Read More

Opening the week, the local bourse rebounded, up 0.39% – the highest single-day gain in the month – recovering some

Read More

In the last trading week, commodities closed flat on the Exchange except for Maize, Paddy rice, and Ginger. Maize topped

Read More

Activity on the local bourse was bearish as the benchmark index fell by 0.47% to settle at 49,190.34 points —

Read MoreFlutterwave, Africa’s leading payments technology company, today announced Google Pay, a mobile payment service, developed by Google, as a payment

Read More

Amazon has announced that it is expanding its renewable energy portfolio globally, with an additional 2.7 gigawatts (GW) of clean

Read More

Remedial Health, a healthtech startup that develops solutions to make Africa’s pharmaceutical value chain more efficient, has raised $4.4 million

Read More

FairMoney, a credit-led mobile banking platform for emerging markets in Africa and Asia, has partnered with Oradian, a cloud-based core

Read More

The Central Bank of Nigeria (CBN) has issued Africave Technologies Limited DBA Kippa, the financial management and payments platform, a Payment Solutions Services

Read More

The International Executive Committee of the All Africa Music Awards (AFRIMA) (https://www.AFRIMA.org), in conjunction with the African Union Commission (AUC),

Read MoreShareholders of Sterling Bank Plc unanimously voted in favor of the creation of a new non-operating holding company (HoldCo) to

Read MoreDecklar Resources (Decklar), and its co-venturer Millenium Oil & Gas Company (Millenium), announced that the 7,800 barrels of crude oil (bbls)

Read More

In the last trading week, Maize and Paddy rice gained respectively while other commodities remained flat on the Exchange. Old

Read More

The pharmaceutical firm, Sterling Biopharma Limited, has introduced a new product called Fejeron Blood Tonic into the Nigerian market to

Read More

Binance (www.Binance.com), the world’s leading blockchain ecosystem and cryptocurrency infrastructure provider has launched a crypto education tour across 5 countries in

Read More

Activity on the Lagos bourse was mixed, albeit with a bullish tilt as the benchmark index edged up slightly higher

Read More

Opportunity through uncertainty: After a stellar GDP growth performance in 2021, Africa finds itself in the midst of remarkable uncertainty.

Read MoreOn September 13 in Abuja, Special Presidential Envoy for Climate John Kerry joined the Government of the Federal Republic of

Read More

Nigerian equities extended losses for the fourth consecutive session as the All-Share Index closed 0.07% weaker to settle at 49,440.21

Read More

Climate disasters and skyrocketing fuel prices have made the need to “end our global addiction to fossil fuels” crystal clear,

Read More

TechPR Nigeria, a Public Relations and Communications firm, has announced the appointment of Felicia Omari Ochelle as the new Chief Executive Officer

Read MoreClickatell has partnered with the Central Bank of Nigeria (CBN) to deliver eNaira banking services to all Nigerians using the USSD channel. The two partners have

Read More

Nigerian blockchain payments startup Bitmama announced a pre-seed extension of $1.65 million, adding to the $350,000 it received last October, thus

Read More

At The Big 5 Construct Nigeria 2022, public and private stakeholders will come together to explore sustainable solutions for the growth of

Read MoreYoung entrepreneurs between the ages of 18 and 35 are invited to submit their business plans through the official submission

Read More

A Memorandum of Understanding was signed on Thursday 15 September in Rabat, Morocco between ECOWAS, the Federal Republic of Nigeria

Read More

The NBS has released its August inflation report to show – Headline rate 20.52% y/y (19.64% in July); Core rate

Read More

Be among ten talented pan-Africanist writers and visual artists who will help mark 20 years of the African Union. Under

Read More

More startups scale up to serve freelance and contract workers Freelancers and contract workers now make up a vast and

Read More

The Economic Commission for Africa (ECA) launched a network for Francophone African journalists, dubbed “AfCFTA Media Network”, to enhance the

Read More

In the last trading session of the week, the domestic bourse succumbed to sell pressure as the All-Share Index declined

Read More

BGI-Research and the Maternal and Child Health Hospital of Hubei Province (MCHH) published whole-genome sequencing research results in npj Genomic

Read MoreAccess Holdings (ACCESSCORP) released its H1 22 audited results after trading hours on Wednesday (14 September). The group reported marginal

Read More

The Bolè Festival, the biggest food and music festival in Port Harcourt, took place a month ago. The festival’s sixth edition

Read More

Ecobank Group has today announced a partnership with AMA Academy, which is the only free-to-use pan-African online learning platform dedicated

Read More

Global analytics leader SAS recently hosted a Summit in Lagos, focused on enabling a new era of financial services in

Read More

Flutterwave merchants can now process payments in eNaira, the Nigerian digital currency issued and distributed by the Central Bank of

Read More

300 women from across Africa have graduated from Binance’s First Blockchain Bootcamp which kicked off in March 2022. The women were selected from

Read More

Pan-African media company, Big Cabal Media, will unveil its first ‘Commerce in Africa’ outlook report at the Future of Commerce 2022

Read More

Pan-African housing development financier Shelter Afrique has extended USD19.5 million (₦8 billion) line of credit to Lagos-based real estate firm, Mixta

Read More

Turaco, the leading insurtech driving mass market insurance adoption, has announced the close of a $10 million Series A equity

Read More

Private company owners who hope that their children will want to take over the family business should prepare themselves, the

Read More

Afro Nation (www.AfroNation.com), the world’s biggest Afrobeats Music festival, has extended its partnership with APO Group (www.APO-opa.com), the leading Pan-African

Read More

On August 30th, the SIBC officially launched its6th edition, welcoming the 43 entrepreneurs selected for the 2022 cohort. These social and inclusive

Read MoreStartups raise record sums to cut food waste The problem of food waste has attracted more attention in recent years,

Read More

According to Kevin Urama, vice president and acting chief economist of the African Development Bank Group (www.AfDB.org), Africa has been

Read More

The African Development Bank (www.AfDB.org) has welcomed 12 new Executive Directors, including five women, for a three-year term. The President

Read More

Nigerian equities opened the week on a weak note, reversing prior session gains as the All-Share Index was 0.14% weaker

Read More

NIGERIA S&P affirmed Nigeria’s long- and short-term foreign and local currency sovereign credit ratings at ‘B-/B’ with a stable outlook.

Read More

African agritech innovators from all four corners of the continent claimed victory in the 8th edition of Pitch AgriHack. The 2022

Read More

In a review of last week’s trading activities, paddy rice and sorghum sustained a 2-week price increase in the open

Read More

As a mission-driven company, M-KOPA’s tremendous growth is rooted in commitment to both commercial and social goals. The report presents

Read More

Ecobank Transnational Incorporated (ETI), the parent company of the Ecobank Group, has appointed Jeremy Awori as the Group’s Chief Executive Officer, to succeed Ade Ayeyemi,

Read More

The World Health Organization (WHO) and partners have launched a roadmap to stop by 2030, bacterial meningitis outbreaks on the

Read More

Following a successful bid process, MainOne (www.MainOne.net), an Equinix Company has been announced as the host of the 12th edition of

Read More

The Lagos Chamber of Commerce and Industry (LCCI), Established in 1888, is a foremost institution in public policy advocacy as

Read More

United Bank for Africa (UBA) released its H1 22 audited results during trading hours on Thursday (8 September). The group

Read More

The Nigerian equities market was bullish today as the All-Share Index (ASI) rose 0.09% to close at 49,695.12 points. UBA

Read More

Nigerian fintech startup NowNow Digital Systems has raised $13M in its seed round for expansion across Africa. The company was

Read More

The National Bureau of Statistics (NBS) released its latest report on capital importation for Q2 ’22. The data was obtained

Read More

Activity on the Lagos bourse was mixed, albeit with a bullish tilt as the benchmark index closed marginally higher (+0.03%)

Read MoreIAA, a global digital marketplace connecting vehicle buyers and sellers, announced it has expanded its service footprint of IAA Transport

Read More

The Creative Business series – Third Edition is around the corner! We are excited to invite you to the Third edition of

Read More

With only one account, business customers can receive funds instantly from their clients in their home country and across Ecobank’s

Read More

The federal government has concluded plans train 2,000 residents in Nasarawa on various skills as part of its commitment to lift 100

Read More

Today, the domestic bourse extended losses from the previous session, bringing the All-Share Index down by 0.69% to close at

Read More

The Business Community is invited to make nominations of deserving individuals, group and/or organisations for the 2022 IoD Nigeria Annual

Read More

To support the growth and sustainability of Nigeria’s livestock industry, IFC announced a partnership with the Nigerian subsidiary of Bar

Read MoreMeta has announced the launch of ‘Creators of Tomorrow’, a new campaign that celebrates emerging talents from around the world

Read More

Today Uber (www.uber.com) announced the launch of multiple new products and features which are going live this month in South

Read MoreNigeria will host Shelter Afrique’s 42nd Annual General Meeting in Abuja, the pan- African housing development financier has disclosed. This follows

Read More

The year is 2022, and it is safe to say we are living in a technocentric world already. There is

Read More

Opening the week, Nigerian equities reversed the three-day winning streak as the All-Share Index closed 0.11% weaker to close at

Read More

During the trading week, we observed mixed performance in the price of grains on the Exchange. Sorghum gained 1.05% while

Read More

Increased taxation weighs on H1 earningsStock Rating: BUYPrice Target: N36.63Price (03-Sep-2022): N19.90Potential Upside / Downside: +84.1%Tickers: GTCO NL / GTCO.LG Guaranty Trust Holding Company (GTCO)

Read More